Author

Zigurat Global Institute of Technology

Blog / Leadership & Transformation

Categories

Financial technology, or Fintech for short, refers to technology-enabled financial solutions.

It is the union of financial services and information technology to make transactions faster, easier to use and more secure.

And though we may think we have Fintech ever since we can speak of modern society, it has actually evolved over distinct eras.

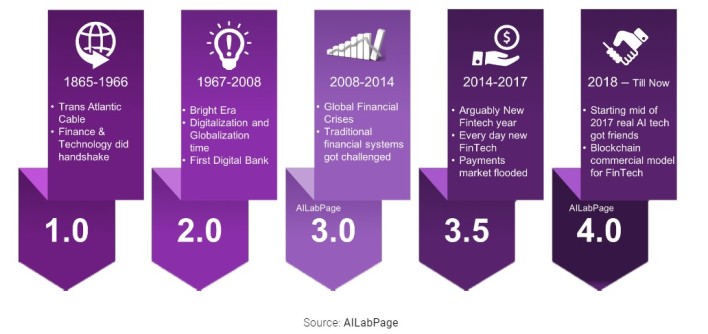

Technology has always played a key role in the financial sector, so from which point onwards can we talk about fintech? According to AILabPage, the key periods in the timeline of fintech are:

Following this table of eras, we can identify the key events of each period.

This is an era when we can first start speaking about financial globalization. It started with technologies such as the telegraph as well as railroads and steamships that allowed for the first time rapid transmission of financial information across borders. The key events on this timeline include first transatlantic cable (1866) and Fedwire in the USA (1918), the first electronic fund transfer system, which relied on now-archaic technologies such as the telegraph and Morse code. The 1950s brought us credit cards to ease the burden of carrying cash. First, Diner’s Club introduced theirs in 1950, American Express Company followed with their own credit card in 1958.

This period marks the shift from analog to digital and is led by traditional financial institutions. It was the launch of the first handheld calculator and the first ATM installed by Barclays bank that marked the beginning of the modern period of fintech in 1967.

There were various significant trends that took shape in the early 1970s, such as the establishment of NASDAQ , the world’s 1st digital stock exchange, which marked the beginning of how the financial markets operate today. In 1973, SWIFT (Society For Worldwide Interbank Financial Telecommunications) was established and is to this day the first and the most commonly used communication protocol between financial institutions facilitating the large volume of cross border payments.

The 1980s saw the rise of bank mainframe computers and the world is introduced to online banking, which flourished in 1990s with the Internet and e-commerce business models. Online banking brought about a major shift in how people perceived money & their relationship with financial institutions.

By the beginning of the 21st century, banks’ internal processes, interactions with outsiders and retail customers had become fully digitized. This era ends with the Global Financial Crisis in 2008.

As the origins of the Global Financial Crisis that soon morphed into a general economic crisis become more widely understood, the general public developed a distrust of the traditional banking system. This and the fact that many financial professionals were out of work, led to a shift in mindset and paved a way to a new industry, Fintech 3.0. So, this era is marked by the emergence of new players, particularly fintech startups, alongside the already existing ones (such as banks).

The release of Bitcoin v0.1 in 2009 is another event that has had a major impact on the financial world and was soon followed by the boom of different cryptocurrencies (which, in turn, was followed by the great crypto crash in 2018).

Another important factor that shaped the face of fintech is the mass-market penetration of smartphones that has enabled internet access for millions of people across the globe. Smartphone has also become the primary means by which people access the internet and use different financial services. 2011 saw the introduction of Google Wallet, followed by Apple pay in 2014.

Fintech 3.5 signals a move away from the western dominated financial world and contemplates the expansion in digital banking around the globe, with improvements in fintech technology.

It puts the focus on consumer behaviour and how they access the internet in the developing world. For example, in China and India, markets that never had time to develop Western levels of physical banking infrastructure and so were open to new solutions more quickly.

This era is marked by an increasing number of new entrants and their last mover advantages.

Blockchain applications as a notary services and open banking are continuing to drive the innovation of the future of financial services. The game changers here are neobanks that challenge the pricing and complexity of traditional banks, while earning customers’ trust through simplified, digital-only experiences and low-to-no fees.

Machine Learning, on its part, is transforming the way people interact with banks and insurance companies, receiving bespoke offers and support. Germany’s N26, for example, relaunched its premium account in 2019 to cater to the specific needs and tastes of its subscribers, such as discounts in coworking spaces and in online travel booking sites.

ML also has security applications: British Revolut, for example, unveiled a new AI solution in 2018 to combat card fraud and money laundering, developing deep insights and predictions around customer behaviour to dynamically identify new card fraud patterns without human intervention.

Another major event in this period is the new wave of integrated payment providers, with platforms that can offer payments as an additional strand to an already comprehensive business management system.

And lately, mainstream use cases for NFTs, like creators strengthening their earning power with digital representations of their contents, or artists ensuring royalty distributions, or NFTs as tickets or membership cards.

As technology is becoming ever more central in the finance industry, we tend to consider banks and fintech startups as opposing forces fighting for their share of the market. The reality is that both sides need each other just as much as they need to compete with each other.

On the one hand, fintech startups have taken funding from banks and often rely on banking, insurance, and back office partners to deliver their core products. Banks, on the other hand, have acquired fintech startups or invested in them to leverage new technology and ways of thinking to upgrade their existing operations and offerings.

Hopefully, this retrospective look into the evolution of fintech will help to sum up the long way we’ve come until today and put into perspective the busy times ahead of us.

One thing is certain: Fintech is growing, and fast. And innovation in fintech is reaching more and more areas of the digital economy.

The increasing number of unicorns (privately held startup businesses with a value of over $1 billion) is an indicator of this.The same applies to dragons, firms that raise $1 billion from investors in a single round (and that are therefore more aggressive companies).

Another indicator of Fintech growth and potential is the enormous amount of global fintech VC investments. In fact, 2021 smashed all records in this domain!

That’s why, if you want to thrive in today’s digital economy, Finetch literacy is a must.

In our Global MBA in Digital Business we cover Fintech’s challenges, solutions and real-world applications with renowned expert Lilia Stoyanov, who devotes an entire academic model to this topic.

Many of our students have been able to apply digital transformation in finance.

"Deloitte estimated that the Fintech industry will be worth USD 213 billion in 2024, but I believe its potential is even bigger due to the incresaed investment in Internet infrastructure during and after the pandemic”, Stoyanov declares.

“Fintech is the future of financial services, but how to select the payment provider that best addresses your needs? That 's the key!”, she then points out.

And that's precisely what she will help you with in our MBA in Digital Transformation with AI, designed to equip professionals like you with the skills to drive innovation, implement AI-driven strategies, and lead businesses through the digital economy with confidence. It's a holistic programme that covers strategy, application, and cybersecurity.

Zigurat Global Institute of Technology